What role does the EEX exchange play in emissions trading?

by Dagmar Dieterle-Witte

Interview with Tanja Listner, Senior Sales Manager, European Energy Exchange AG (EEX)

1. What is the EU Emissions Trading System and why is it relevant to the industry?

The aim of the EU Emissions Trading System, or EU ETS for short, is to put a price on climate-damaging emissions. It is a market-based instrument designed to gradually reduce climate-damaging emissions in a cost-effective and sustainable manner. The EU ETS was launched back in 2005 as the first multinational trading system. It is regarded worldwide as a pioneer and model for other emissions trading markets. The EU ETS sets an upper limit on CO2 emissions in certain sectors, known as the ‘cap’. For every tonne of carbon dioxide emitted, companies must present a certificate, known as an emission allowance (EU Allowances – EUA).

The aim of the EU Emissions Trading System, or EU ETS for short, is to put a price on climate-damaging emissions. It is a market-based instrument designed to gradually reduce climate-damaging emissions in a cost-effective and sustainable manner. The EU ETS was launched back in 2005 as the first multinational trading system. It is regarded worldwide as a pioneer and model for other emissions trading markets. The EU ETS sets an upper limit on CO2 emissions in certain sectors, known as the ‘cap’. For every tonne of carbon dioxide emitted, companies must present a certificate, known as an emission allowance (EU Allowances – EUA).

These certificates enter circulation in two ways: firstly through auctions and secondly through free allocation. Once the emission allowances are in circulation, they can be traded, including on the European Energy Exchange (EEX). Those who avoid emissions can save costs or sell surplus emission allowances. This creates a market price for CO2, which provides an economic incentive for innovation in climate protection.

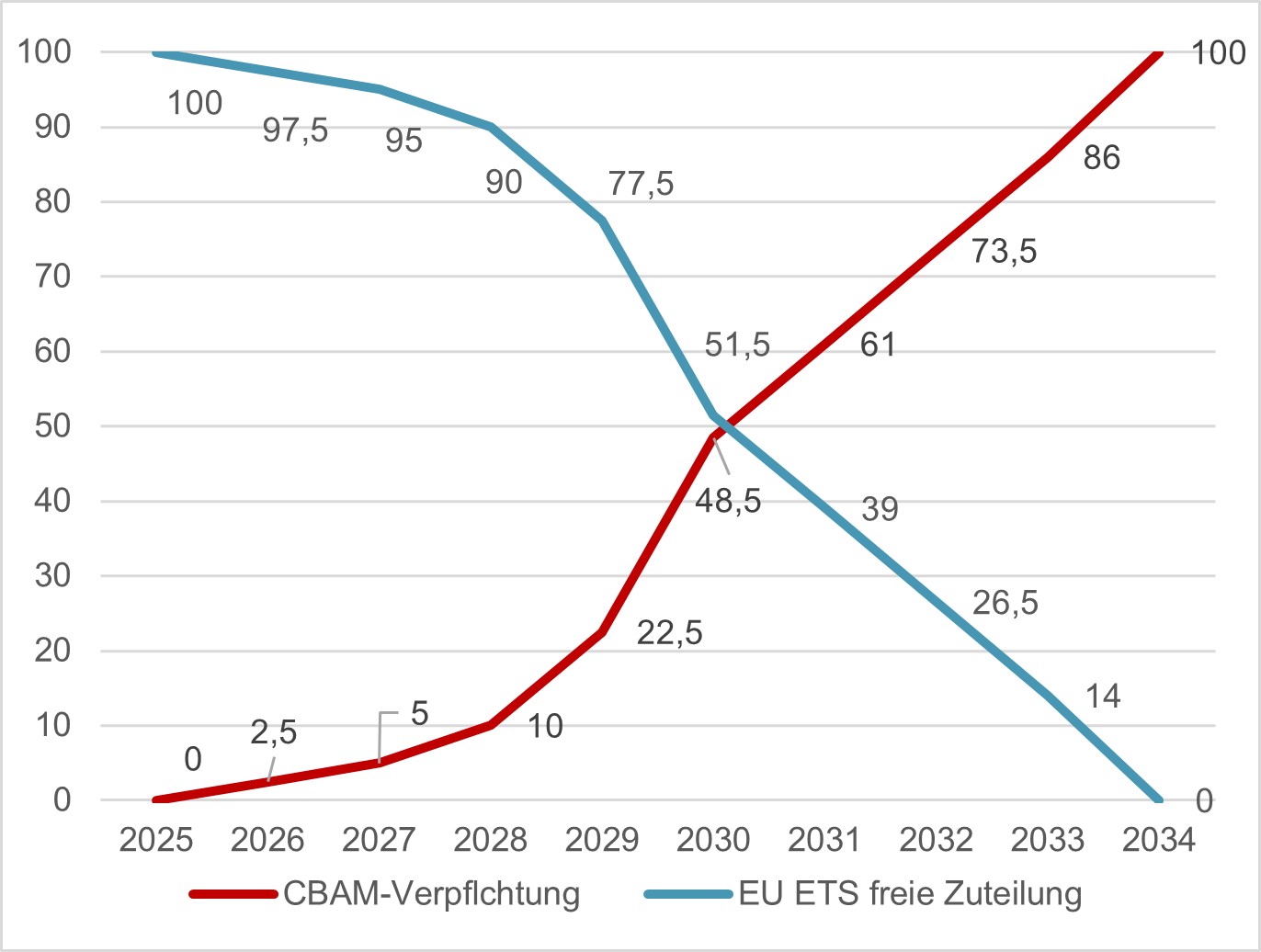

The EU ETS is relevant to the steel industry for several reasons. As an energy-intensive sector, steelworks generate high levels of CO₂ emissions and must hold an EU emission allowance for every tonne of CO₂ emitted. Until now, free allowances have been allocated to the industry for this purpose. However, this free allocation is being phased out and will come to an end in 2035. With the introduction of the Carbon Border Adjustment Mechanism (CBAM), steel importers will have to pay the same price. The steel industry will therefore have to purchase additional allowances to meet the requirements of the European emissions trading scheme. The price of CO₂ is expected to rise further, thereby increasing the price risk for companies. It is therefore important to start addressing risk hedging now.

2. What impact will the CBAM regulation have on the steel industry?

2. What impact will the CBAM regulation have on the steel industry?

The Carbon Border Adjustment Mechanism (CBAM) has been in force since January 2026. This mechanism was developed to protect companies subject to the EU Emissions Trading Scheme from competitive disadvantages. Companies that import steel into the EU, for example, must from this year onwards purchase allowances that reflect the emissions generated by their production. This is intended to ensure that imported products are subject to similar climate protection costs as those manufactured within the EU.

In line with the reduction in the free allocation of emission allowances, the CBAM share is increasing (see Figure 1). For many steel producers, however, the EU ETS is not uncharted territory, as they have long been required to meet permit obligations. Even though these were previously allocated free of charge, the permit price was already relevant in the past due to the possibility of selling them and thus generating income. In future, however, emission allowances will primarily appear as costs, which further increases the relevance of prices. Companies must therefore consider how they will manage this price risk in the coming years. The level of the CBAM price can already be seen today on the EEX, as we publish a CBAM reference price every Friday.

3. What role does the EEX exchange play in emissions trading?

EEX is Europe’s leading energy exchange and operates electronic marketplaces for the wholesale trading of electricity, natural gas, emission allowances and other energy-related products. We have been involved in emissions trading since the very beginning. On EEX, trading participants can buy and sell emissions allowances, thereby fulfilling their obligations under the EU ETS. We refer to those companies that are directly admitted to trading on the exchange as trading participants. Our participants include energy suppliers, industrial companies, specialist trading firms, brokers and banks – more than 500 companies from across Europe and beyond. It is also possible to participate in exchange trading indirectly. This is done via so-called intermediaries, i.e. companies that offer access to the exchange as a service, such as brokers and banks.

Graph: Source: European Commission, figures in per cent

Instead of free allocation, emission allowances are increasingly being issued to the market through auctions – with EEX serving as the central auction platform in Europe. Since 2010, we have been organising so-called primary market auctions for 25 EU Member States, thereby generating revenue for the participating countries’ climate protection programmes. On the EEX secondary market, allowances that are already available on the market are traded. Here, trading can take place with short-term delivery of the allowances on the so-called spot market, or it is possible to buy or sell allowances on the futures market for the long term and hedge against price fluctuation risks over the long term.

Furthermore, EEX plays a central role in various emissions trading systems worldwide. Through our subsidiary in the USA, we operate emissions trading markets in North America and support the auction system in New Zealand. Since 2021, EEX has also been the sales platform commissioned by the German Federal Environment Agency for the national emissions trading scheme (nEHS) in Germany.

4. How does trading on the EEX work and what are the benefits?

Trading on the EEX is conducted entirely electronically and follows a clearly defined, regulated process. Trading on the exchange is also anonymous, which ensures that all companies are treated equally. Buyers and sellers therefore do not see who their counterparty is, but only the bids and offers in the exchange’s order book. The price is determined by the meeting of supply and demand. When a seller’s offer matches a buyer’s bid, a trade is executed and the transaction is concluded. The advantage of anonymity is that prices are free from distortions and are therefore of a higher quality than, for example, a bilateral transaction, where the price may be subject to additional influences.

All participants admitted to the EEX must comply with various rules, such as the Exchange Rules, the Trading Conditions and the Admission Rules. In this way, we ensure that trading and admission are non-discriminatory and remain fair. In addition, there is a dedicated trading surveillance unit, an independent body established under the Exchange Act, which monitors trading on all EEX markets on a daily and comprehensive basis. EEX promotes transparency by publishing market data on traded prices and volumes, both on its website and in the form of data products, through which historical data, for example, is available. After every trade is concluded, our clearing house, European Commodity Clearing AG (ECC), guarantees the secure settlement of all transactions. Should a trading participant default, the clearing house steps in and assumes the obligations arising from the trade, namely payment and delivery.

All participants admitted to the EEX must comply with various rules, such as the Exchange Rules, the Trading Conditions and the Admission Rules. In this way, we ensure that trading and admission are non-discriminatory and remain fair. In addition, there is a dedicated trading surveillance unit, an independent body established under the Exchange Act, which monitors trading on all EEX markets on a daily and comprehensive basis. EEX promotes transparency by publishing market data on traded prices and volumes, both on its website and in the form of data products, through which historical data, for example, is available. After every trade is concluded, our clearing house, European Commodity Clearing AG (ECC), guarantees the secure settlement of all transactions. Should a trading participant default, the clearing house steps in and assumes the obligations arising from the trade, namely payment and delivery.

The steel industry is currently at the heart of one of the greatest transformations of our time and plays a significant role in decarbonisation. Please feel free to contact us if you have any questions regarding access to and emissions trading on the EEX.

Tanja Listner, Senior Sales Manager, EEX (Contact: tanja.listner@eex.com)